🤑 Smart Money in Creator Economy - March 13 to March 19

Fundraising and exits of the #CreatorEconomy - what happened last week?

Hi, it’s Ange!

Welcome on 🤑 Smart Money in Creator Economy, the new format of Passion & Creator, the media hub about emerging trends in the exciting vertical of the Creator/Passion Economy.

Every week on Money flows in Creator Economy, receive the last fundraising and exits of the Creator Economy!

Dear investor friends, it’s time to pick new deal flow in it 🤩

Dear founders, discover who invest in this amazing vertical, and maybe in your (next) Creator Economy startup.. 😉!

Feel free to reach out if you’d like to share comments or questions. Don’t forget to like this post above and share it with your friends and colleagues.

😶 If the images are not displayed, press "Show blocked content" at the top left of this email.

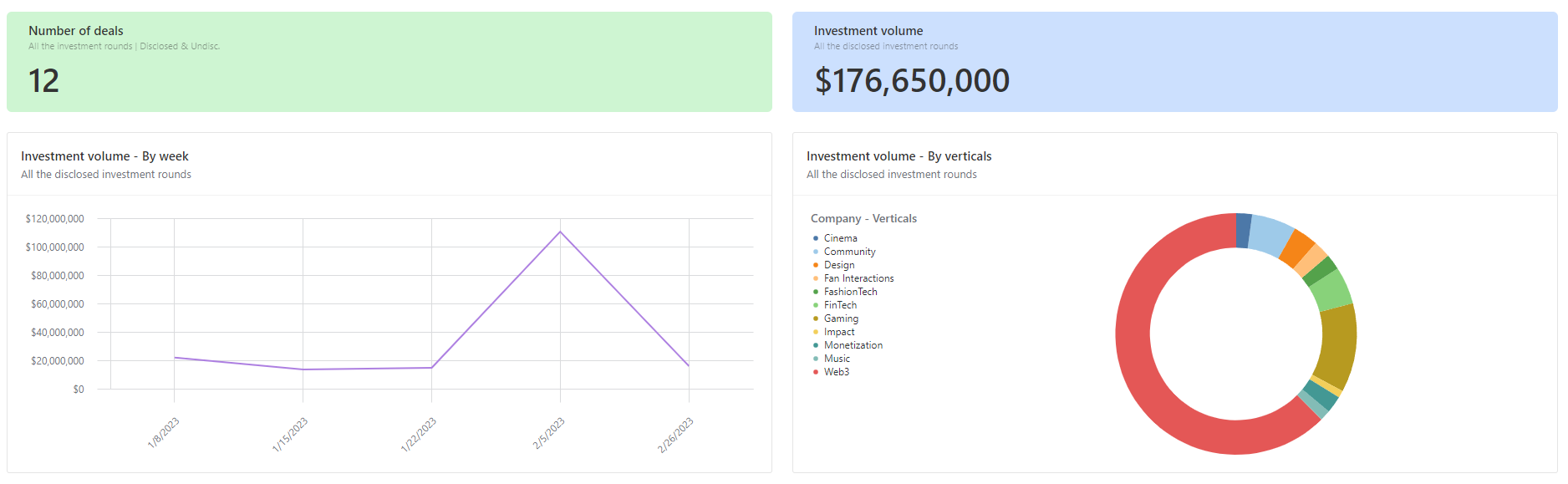

💰 A light week, dedicated to GameFi & influence marketing with $32M raised on 2 rounds!

🟪 Tilia by Linden Lab (2022 / USA 🇺🇸)

#FinTech / #Gaming: enables to embed creator monetization solutions in games

Transactions volume-based revenue model / B2B customer approach

Raised an $22M Venture round

Led by JP Morgan Payments, a specialist branch of the investment bank and the crypto & fiat-focused stock exchanges Dunamu.

🟪 One Impression (2017 / India 🇮🇳) - 15 Mar

#InfluenceMarketing: connects creators to brands through influence marketing campaigns

SaaS revenue model / B2B/B2Creators customer approach

Raised a $10M Series A round, with a $70M post-money valuation

Lead by the gaming company Krafton.

We will find the new 2 deals with the other 53 listed deals of 2023, in the new Creator Economy deals database:

NB: I am currently on a last check on the deals of 2022. Once finished, you’ll have you access of all deals of 2022 (+480 deals, +470 companies, +590 investors and +20 buyers)!

Quick review about the web3 side of the Creator Economy of 2023.

Like as in the previous article of “Smart Money in Creator Economy”, the Creator Economy has clearly taken profit of the Web3 wave in 2022. Now in 2023, the investment volume difference is stunning: 80% decrease in deal volume, and more than $2B in dollars value. The interest from investors is dead? No, because we have to put context about the 2022 results.

In comparison, just by checking the data, in 2022, a majority of solutions was focused on the NFT value chain, in the hope to help creators, from the long-tail to celebrities to take the opportunity to gather their communities around collections and make money. We had the protocols (Burnt finance, Metaplex Studios), the minting, the community building (TRLab), the applications for verticalised NFT (Art platforms like LaCollection or TRLab, or music NFTs like Unblocked) , the exchanges of NFTs (OpenSea, Flip, & blockchain-based IP (Anotherblock, POAP), the analytics with (Cryptoslam, Dune Analytics)the metaverses assets (Nifty Island) to help creators welcome their community on their digital real estate properties and others universes. In 2023, the NFT interest in Creator Economy is very niche: the digital fashion, the digital assets for games, or music NFT, or the decentralized movie distribution. It seems that the superfan behavior will potentially the consumer to pay for NFTs in these hard times for cryptos. Aside NFT, the web3 gaming (the Play-To-Earn as a flagship), that keep interest from their investments, but like the rest, the investment volume follow the crypto winter. I spoke a lot about the web3 gaming in different articles, so let’s just say the the gaming digital assets is the subject that keep interest for the moment for the investors.

Furthermore, just in terms of figures, we see that is the investor behavior is completely different. Last year, money seems flow everywhere. It was a time where Web3 juggernauts raised money at this time for growth stages ($350M for Animoca Brand to build new creator monetisations in games, $300M for OpenSea to help creators monetize their collections, $150M for Genies to create the social avatars for celebrities and regular creators …) to either directly help creators, and enhance their infrastructure around them. Even if their majority of the deal went in the early-stage (+55% of deals in Pre-Seed & Seed for $378M), the VC & some PE pushes their best bets on venture & growth stages (36% of deals in the Venture stages for $1.1B; 8% of deal in Growth stages for $955B). Now, VCs keep the money in the pocket and only makes small bets. Aside a 100M Series A on Tokhit, all the deals of 2023, almost all the deals are Seed bets, below the $10M mark.

But I think it’s too soon to tell that the Web3 Creator Economy will be stay calm: the next two quarters will be interesting. Lot of companies last year, raised their Pre-Seed and Seed in Q1 & Q2. If we assume they managed to slowdown their burn rate (at this time, most companies could thinking about raising between M+12 & M+18), either the best companies will raise their next round in Q2 or Q3, early July or September of 2023 their Series A (at best) or Seed extension (at worst), or the unlucky ones will hold the line all the year with the first funding, or dies by lack of money.

The web3 revenue models, often based on transaction volume, require a high engagement of the consumers to be sustainable. Consequently, these current times are hard for thees startups, but I think that the most sustainable or attractive for communities will stay online.

👼 Who are the most active business angels?

When it comes to finding tech investors, we have two entities in mind: the Venture Capitalist & the Business Angel! While finding key infos about VC could seems “easy” due to they are legal entities, and several people, a website, public content about their investment thesis, and their company portfolio. Ok fine!

But when it’s about the business angels, it’s another game, and everything seems more blurry! Each angels manages singularly its visibility, so that it’s tough for companies to know to who target when they are ‘re thinking about the first ticket, especially in the “niche” vertical of the Creator Economy.

So, like in every article of “🤑 Smart Money in Creator Economy”, you’ll find the most active investors of this powerful category, the business angels, who launch the VC game of the majority of the tech ecosystem.

Like in every vertical, you have a broad typologies of angels. In Creator Economy, you’ll find startups founders and operators, offering vertical and/or functional expertise and network; investment professionals managing their own private investments, acting like a “personal VC”, and other specific types of angels, tailored for the Creator Economy.

Among them, you’ll find public personalities and athletes, offering their main asset, visibility to help on customer acquisition, brand awareness, and network for key partnerships, and the entertainment executives, like movie talent agents, are notorious about holding the best rolodex of the local and/or international entertainment industry.

So, let’s see who are most active creator economy angels in 2022 and 2023.

👩💻 The tech companies founders/operators

Kevin LIN (🇺🇸 | Metatheory, ex-Twitch): 9 deals, including a deal since January 1

Sébastien BORGET (🇫🇷 | The Sandbox): 7 deals

Justin KAN (🇺🇸 | Rye, Fractal, ex-Twitch): 5 deals

Sandeep NAILWAL (🇦🇪 | Polygon): 5 deals

Do KWON (🇰🇷 | TerraForm): 4 deals

Gabby DIZON (🇵🇭 | Yield Guild Games): 4 deals

Roham GHAREGOZLOU (🇺🇸 | Dapper Labs): 4 deals

Scott BELSKY (🇺🇸 | Adobe): 4 deals, including a deal since January 1

Kun Gao (🇺🇸 | Crunchyroll/GGWP): 3 deals

Mark Pincus (🇺🇸 | Zynga): 3 deals

Patricio Worthalter (🇦🇷 | POAP): 3 deals

Siqi Chen (🇺🇸 | Runway Financial): 3 deals, including a deal since January 1

Stani Kulechov (🇬🇧 | Aave): 3 deals

Steven Galanis (🇺🇸 | Cameo): 3 deals

Thomas Vu (🇺🇸 | Riot Games): 3 deals

Trevor McFedries (🇺🇸 | Brud/Friends with Benefits): 3 deals

⚽️ The Athletes

Mario GÖTZE (🇩🇪 | FIFA): 4 deals, including a deal since January 1

🤵 The “Public personalities”

Mark CUBAN (🇺🇸): 5 deals

Paris HILTON (🇺🇸): 4 deals

📽 The Entertainment executives

Michaël OVITZ (🇺🇸 | CAA): 3 deals

👩💼 The VC & PE professionals

Mike DUDAS (🇺🇸 | 6th Man Ventures): 4 deals

Santiago Roel SANTOS (… | ParaFi Capital): 4 deals

Balaji SRINIVASAN (🇺🇸 | a16z): 3 deals

Holly LIU (🇺🇸 | PKO Investments): 3 deals

Patrick LEE (🇺🇸 | PKO Investments): 3 deals

Alan HOWARD (🇬🇧 | Brevan Howard Asset Management): 3 deals

🖋 Want to know more info about these investors: click here to have access to the database

That’s it for today!

Do not hesitate to reach on Twitter or Linkedin if some content really touched your curiosity, or if you want to suggest your sources 😎

If you would like to have the next one in your inbox next week, subscribe to it 👇 :

If you like Passion & Creator and want to help it grow, please share it to your colleagues, followers and friends.

See you next time 🙋🏿♂️ !

Ange Michael AHYI